To get you started, Leon encourages taking a moment at the beginning of the year to reflect on your finances. “When you think about your money, do you feel stressed or anxious?” he asks. “If so, what are your key stress points and how can you address them?”

Even small steps can make a difference. Learning about interest rates and savings options, comparing different providers, or reviewing unused subscriptions and memberships are all ways to become more aware of your finances and make informed decisions.

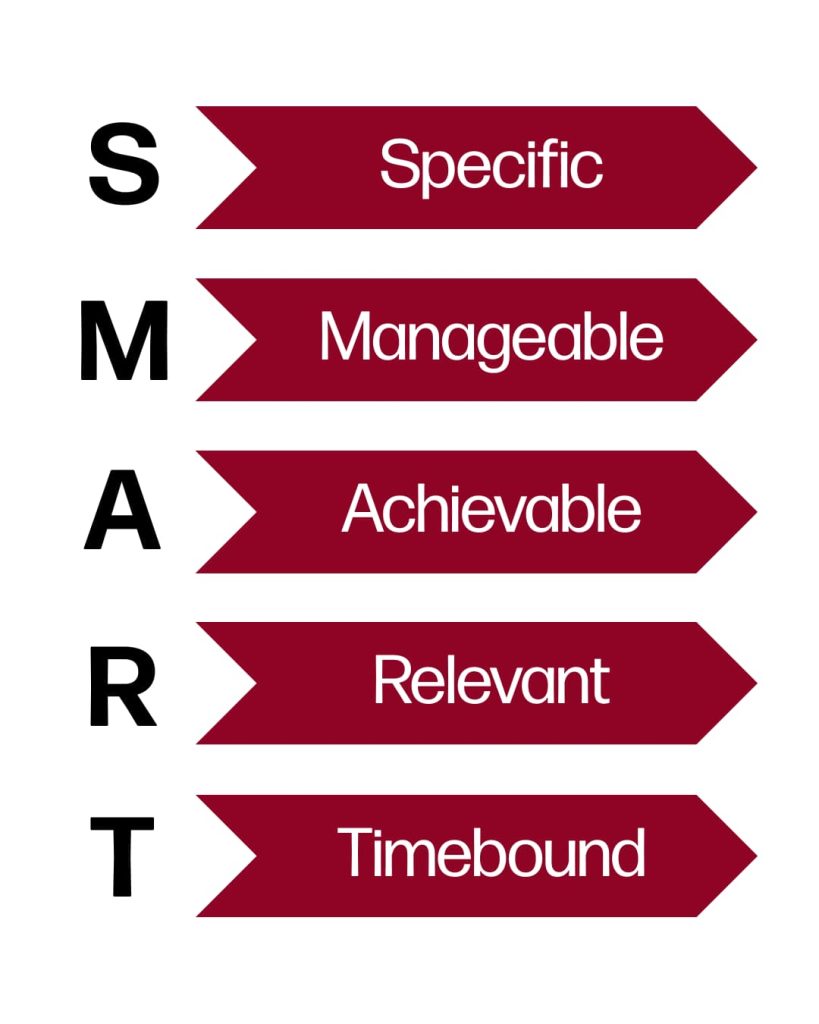

Set SMART financial goals

Leon also suggests setting SMART financial goals for 2026. “SMART is an acronym used by many businesses that stands for specific, measurable, achievable, relevant and timebound. It helps you come up with a plan you can actually use. For example, don’t just plan to save money in 2026, decide the specific amount to set aside each month and make it measurable by tracking your progress or using automatic transfers, if helpful.”

He adds: “This needs to be achievable, so make sure the amount you choose suits your monthly income and costs such as rent or mortgage and bills. To stay motivated, match your saving goals to something that’s relevant to you – such as money towards a holiday or a deposit for a home. And don’t forget to set a deadline, say 31st December 2026, to make it timebound.”

However, Leon reminds us to stay flexible. “If something goes wrong with your car and you have to dip into your ‘future home’ account to cover it, don’t beat yourself up about it. The most successful business plans are the ones that can change in response to the real world.”

2026: The year you become a star saver

Beulah Antonin is Mortgage & Protection Advisor at Charterhouse Mortgages and Protection, part of the Quilter Financial Planning Group. Beulah encourages us to start saving some money in 2026. “Every little counts, so just start!” she enthuses. “Whether it’s £10 or £100, every amount counts. Keep it consistent, build the savings muscle and then increase your savings bit by bit!”

To motivate yourself, think about how you want to be living in ten, twenty or even thirty years’ time.

“Whatever you do now, make sure your future self will be grateful!” says Beulah. “As they say, the best time to plant a tree is 20 years ago, so whatever your age, plant that seed sooner rather than later.”

Dr Tom Mathar, Head of Money:Mindshift, agrees. “Reflect on whether your spending decisions align with the kind of person you want to be now, and in the future.”

Tom also recommends waiting for a full 24 hours before making any non-essential purchase over a set amount. “This simple delay moves the decision from the emotional, impulsive brain to the rational one.”

Wait 24 hours before making any non-essential purchase over a set amount. This simple delay moves the decision from the emotional, impulsive brain to the rational one.Dr Tom Mathar, Head of Money:Mindshift

Embrace financial education and lifelong learning

Sam Hillman is the Reward Director at Quilter, responsible for all aspects of compensation and benefits for colleagues across the Group. He is a strong believer in the value of financial education.

“Learning more about money can make a big difference to how we understand and manage things like budgeting, spending, saving, and planning for the future,” he says. “From my perspective working within a Reward function, it’s important that our employees understand our reward framework. This includes salary, pension and benefits, so they can feel more in control, make decisions with confidence and make the most of the benefits to suit their own personal needs. This requires financial knowledge and understanding, which in turn can reduce stress and lead to better peace of mind.”

If your employer doesn’t offer this, you can find your own routes to understanding money, Leon reminds us. “As well as bringing impactful money education to schools, colleges and community spaces, Money Ready offers online resources at the Money Ready Learning Hub where you can pick up expert tips when you need it.”

Dr Tom thinks of financial education is a form of psychological protection. “It reduces the anxiety and fear that often accompany money decisions,” he says. “When you understand money, you convert vague, scary unknowns into simple, actionable steps. Knowledge empowers you to make decisions based on evidence rather than emotion.”

Try to spend with intention

Finally, our experts recommend that you set the goal of spending with intention.

“This means your money leaves your hands because you decided it should,” Dr Tom says. “It’s about asking: will this purchase add to my contentment, today or in the future?”

Beulah suggests taking time to identify what you really enjoy spending money on. “For me, I love holidays and experiences,” she says. “By prioritising what brings me the greatest joys I’m able to not feel guilty when I do put my money towards these areas. It isn’t about splurging or denying, it’s about knowing what you value and what you actually want to use your money for.”

And that takes us back to the start – what do you want from your money in 2026?

“By identifying the things we want in our lives, whether that’s more confidence in our money or a particular item we hope to buy,” says Leon, “we can take steps towards understanding our money with some help from financial education along the way.”

Keep an eye out for our Cost of Not Knowing campaign launching next week for more information and tips to help you reset your money mindset for 2026 and beyond.

Visit the Money Ready Learning Hub

Have a question about borrowing or budgeting, earning or saving? Check out our knowledge base articles.